August 19, 2025

The 2026 Employer Health Care Strategy Survey gained valuable employer perspectives on health care and collected the myriad ways that employers are combatting rising costs while offering quality plans and programs. Despite the unfavorable cost environment, coupled with growing workforce health risks and demand for more services, employers will continue to invest in employee health and well-being – albeit with an increasingly discerning eye on outcomes and performance.

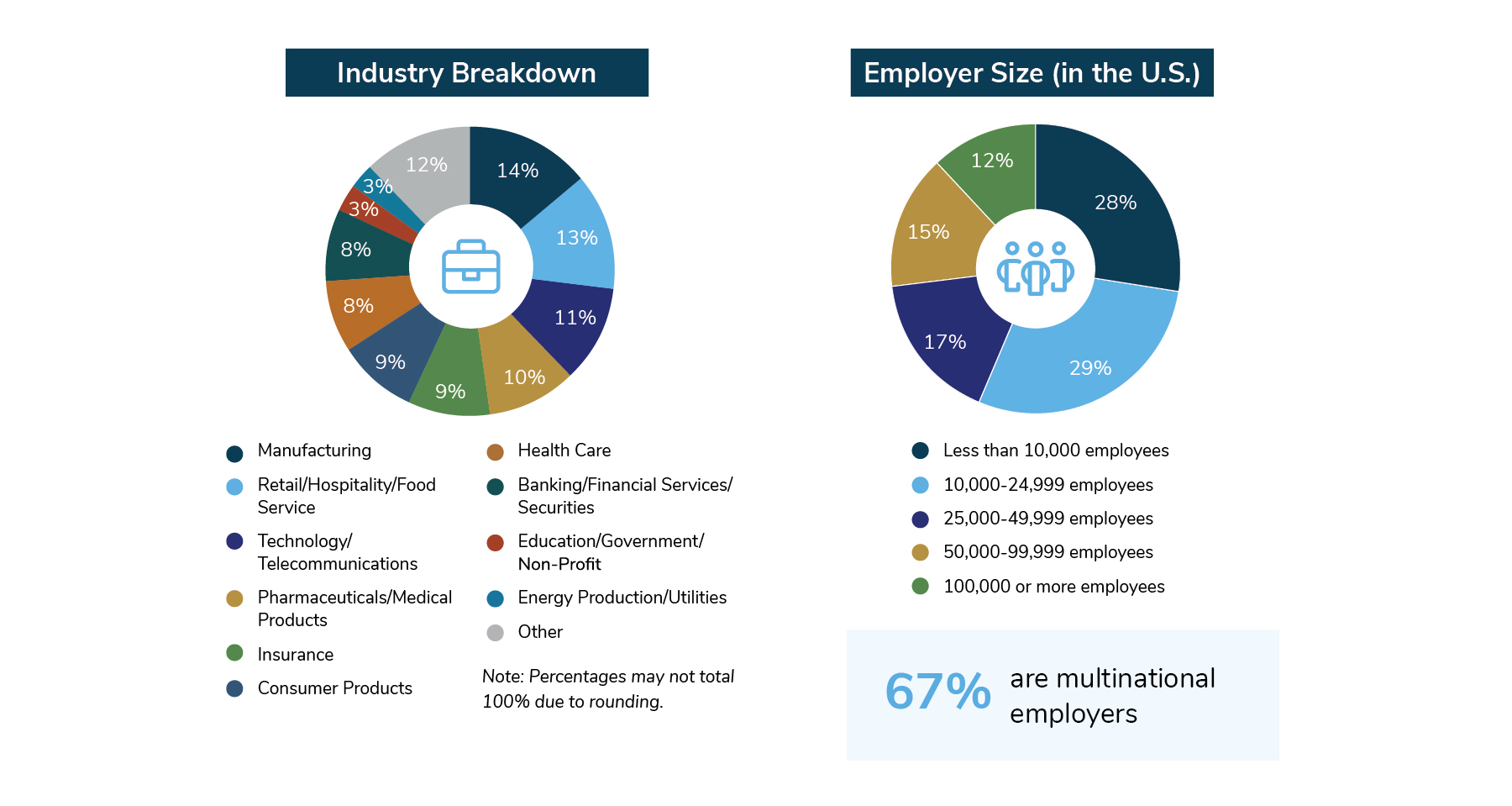

Fielded in June and July 2025, the survey was completed by 121 employers that cover a total of 11.6 million lives. The companies that completed the survey are diverse from an industry and workforce size perspective, as detailed in Figure 1 below.

Additionally, a subset of employers took part in interviews to complement the findings of the survey. The wisdom and guidance that emerged during those conversations helped shape how the data are interpreted in the full report.

The report is divided into the following sections:

- Executive Summary

- Part 1: Health Care and Pharmacy Costs

- Part 2: Health Care Strategy and Plan Management

- Part 3: Health Care Delivery

- Part 4: Health Care Program Design

- Part 5: Pharmacy Strategy and Design

- Part 6: Health Care Policy Perspectives

- Part 7: Global Health Care Costs

- Full Report

- Chart Pack

Ellen Kelsay, President and CEO of Business Group on Health, and the entire Business Group team thank our members for their participation in this project. Your support provided us with rich data and thoughtful insights into the future of employer-sponsored health care.

Citations

Before referring to or using this survey report in any way, you must receive permission from Business Group on Health. Please contact [email protected].

Suggested citation for this survey report:

Business Group on Health. 2026 Employer Health Care Strategy Survey. August 2025. Available at: https://www.businessgrouphealth.org/resources/2026-Employer-Health-Care-Strategy-Survey.

-

Intro2026 Employer Health Care Strategy Survey

-

Executive Summary2026 Employer Health Care Strategy Survey: Executive Summary

-

Part 1Health Care and Pharmacy Costs

-

Part 2Health Care Strategy and Plan Management

-

Part 3Health Care Delivery

-

Part 4Health Care Program Design

-

Part 5Pharmacy Strategy and Design

-

Part 6Health Care Policy Perspectives

-

Part 7Global Health Care Costs

-

Full Report2026 Employer Health Care Strategy Survey: Full Report

-

Chart Pack2026 Employer Health Care Strategy Survey Chart Pack