August 20, 2024

The role of a HR/Benefits leader has never been more complex and demanding. The 2025 survey results highlight the challenges employers face. Based on the findings of this survey, the following emerged as top focus areas among employers.

-

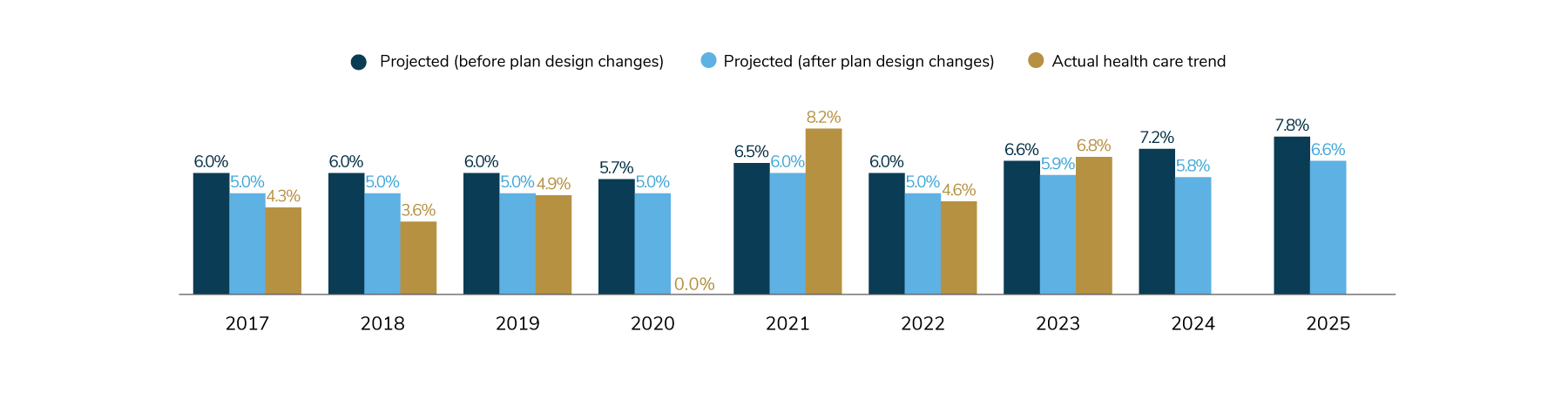

1 | Health care costs are expected to grow at the highest rate in a decade.

Since 2022, the projected increase in health care trend, before plan design changes, rose from 6% in 2022 to almost 8% for 2025. Even after plan design changes, actual health care costs continued to grow at a rate exceeding pre-pandemic increases. These increases point toward a more than 50% increase in health care cost since 2017. Moreover, this health care inflation is expected to persist and, in light of the already high burden of medical costs on the plan and employees, employers are preparing to absorb much of the increase as they have done in recent years.

Figure 1: Median Increase in Health Care Trend (Actual and Projected), 2017-2025

Figure 1: Median Increase in Health Care Trend (Actual and Projected), 2017-2025

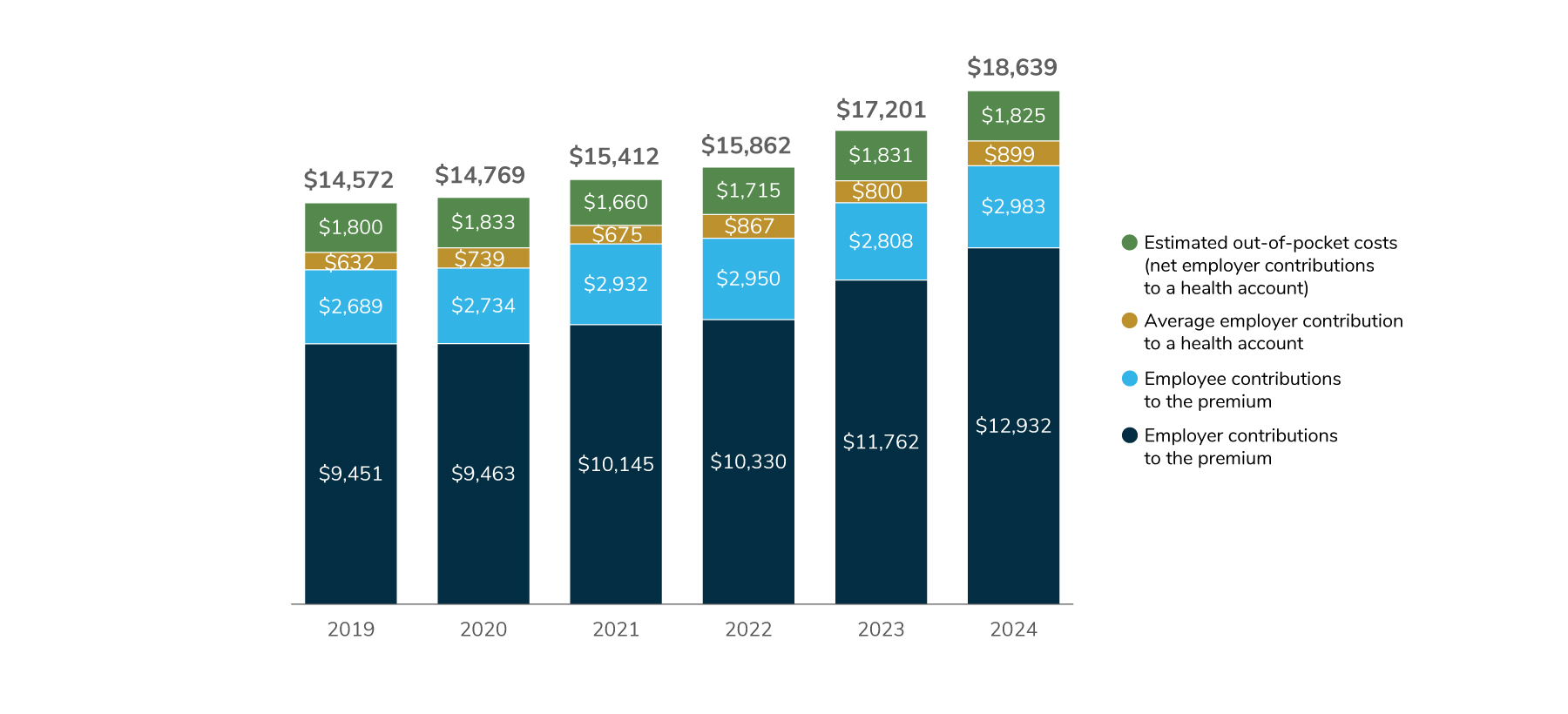

Figure 2: Employer and Employee Contributions to Health Care Costs, 2024

Figure 2: Employer and Employee Contributions to Health Care Costs, 2024 -

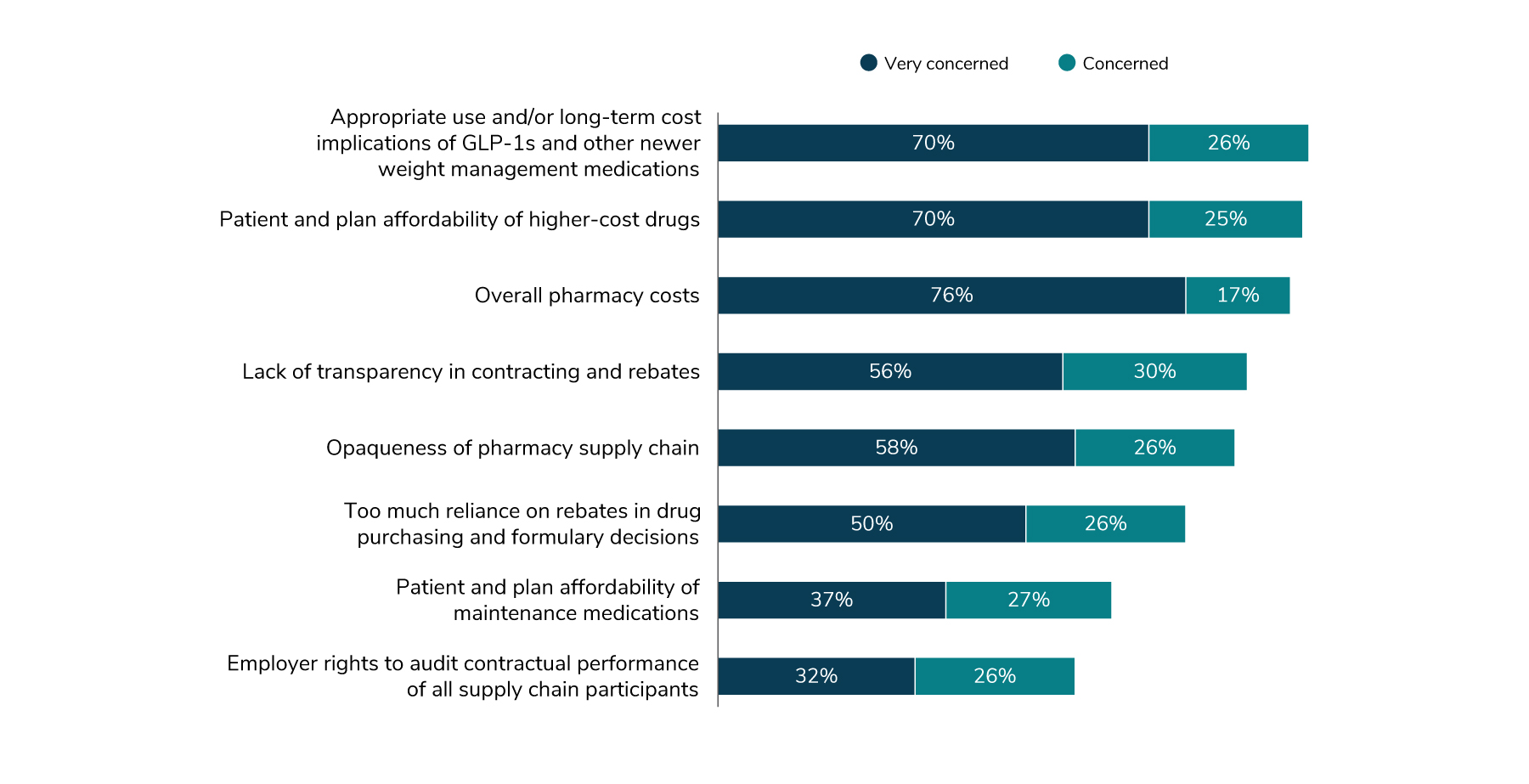

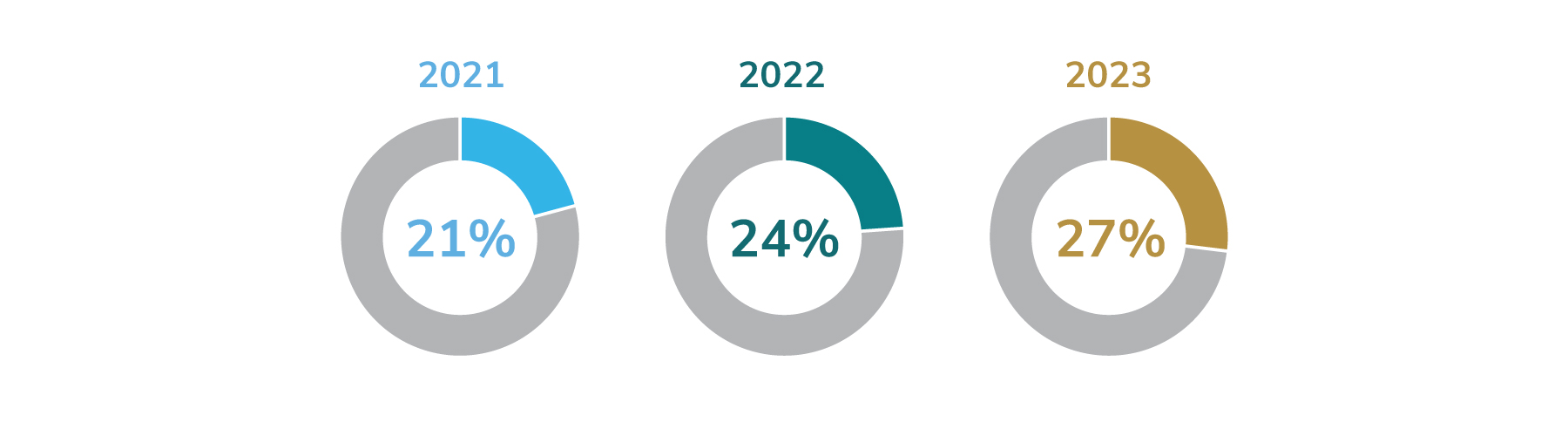

2 | Pharmacy costs are largely responsible for overall increases and consume a growing share of the health care budget.

Between 2021 and 2023, the median percentage of health care dollars spent on pharmacy has jumped from 21% to 27%, suggesting that nearly all of the health care cost increase noted above is related to pharmacy cost. Therefore, it is not surprising that 76% of employers are “very concerned” about overall pharmacy cost. Furthermore, 58% are very concerned about the opaqueness of the pharmacy supply chain and 56% are very concerned about the lack of transparency in pharmacy contracting and rebates. Finally, only 1% of employers think that the prescription drug market is competitive enough to keep prescription drugs affordable, a further decline from 5% who thought so in 2023. The majority of employers call for a combination of market and government reform to curb drug prices.

Figure 3: Pharmacy Benefit Concerns, 2024

Figure 3: Pharmacy Benefit Concerns, 2024

Figure 4: Percentage of Health Care Spend on Pharmacy Overall (Median), 2021-2023

Figure 4: Percentage of Health Care Spend on Pharmacy Overall (Median), 2021-2023

Figure 5: Perspectives on Whether the Prescription Drug Market Is Competitive, 2023-2024

Figure 5: Perspectives on Whether the Prescription Drug Market Is Competitive, 2023-2024 -

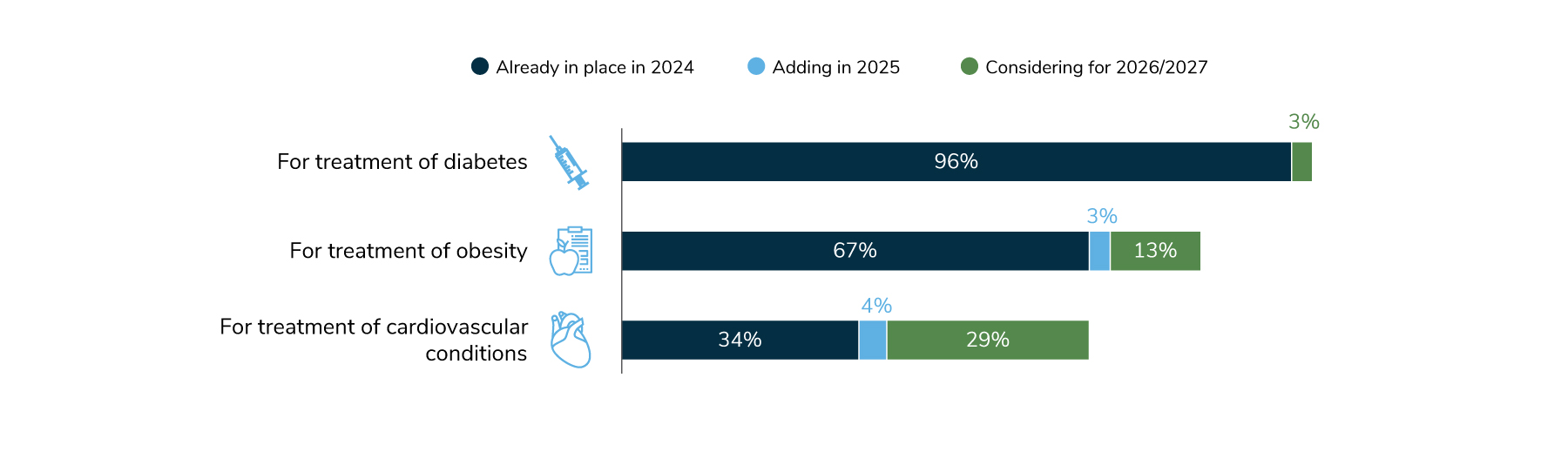

3 | Employers are seeing cost pressures from GLP-1 medications, which are considered a top driver of health care costs this year.

Seventy-nine percent of employers have seen an increase in interest in obesity medications – including GLP-1s – among their covered members. This may be driven by more employees deemed eligible for coverage for these medications: While they have been a standard for treatment for diabetes (covered by 96% of employers), coverage is expanding to other conditions, namely obesity (67% in 2024) and cardiac conditions (34%). With demand rising and more patients being eligible, it is no surprise that 96% of employers worry about the long-term cost implications of these drugs. Although GLP-1 medications are showing near-term promise for the treatment of obesity and other conditions, their cost is concerning. When asked which strategies employers would deploy to reduce overall health care costs, 52% would either immediately implement or strongly consider reducing coverage for GLP-1s (Figure 7).

Figure 6: Coverage of GLP-1s, 2024-2027

Figure 6: Coverage of GLP-1s, 2024-2027 -

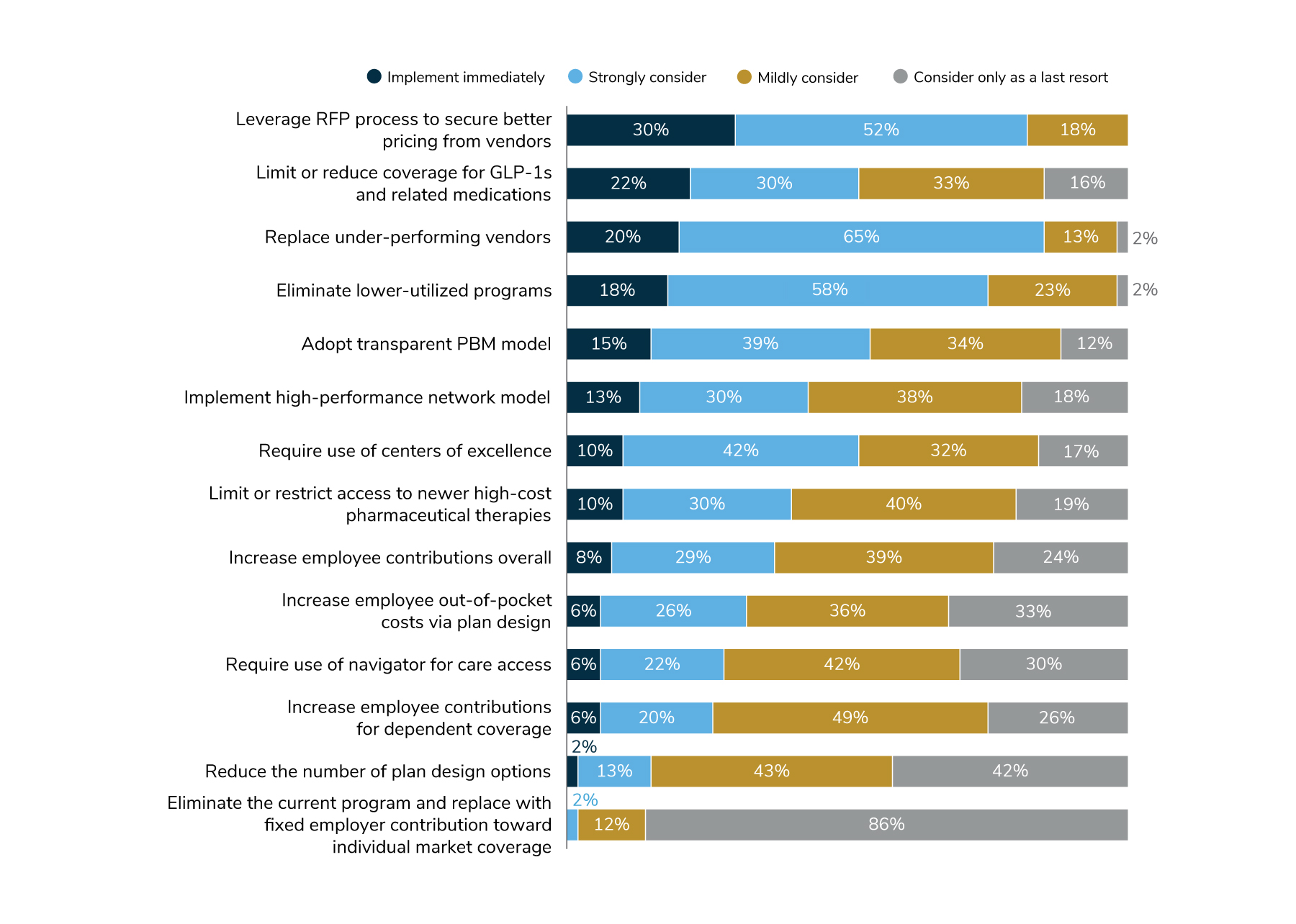

4 | Managing and reassessing vendor partnerships are at the center of employers’ plans to address costs and improve performance. Employers are reassessing the quality and effectiveness of their partnerships and looking to integrate their benefits to reduce costs and simplify the member experience.

Figure 7 shows the major levers employers would pull, if necessary, to keep health care costs flat. Employers would redouble efforts focused on vendor performance, leveraging the RFP process to get better pricing from vendors and ending arrangements with underperforming partners. Employers also see non-traditional health plans and transparent PBM programs as additional in their cost-cutting strategies, along with tighter management of cost drivers such as GLP-1s and eliminating ineffective programs.

Figure 7: Strategies Employers Would Consider for Reducing Costs, 2024

Figure 7: Strategies Employers Would Consider for Reducing Costs, 2024 -

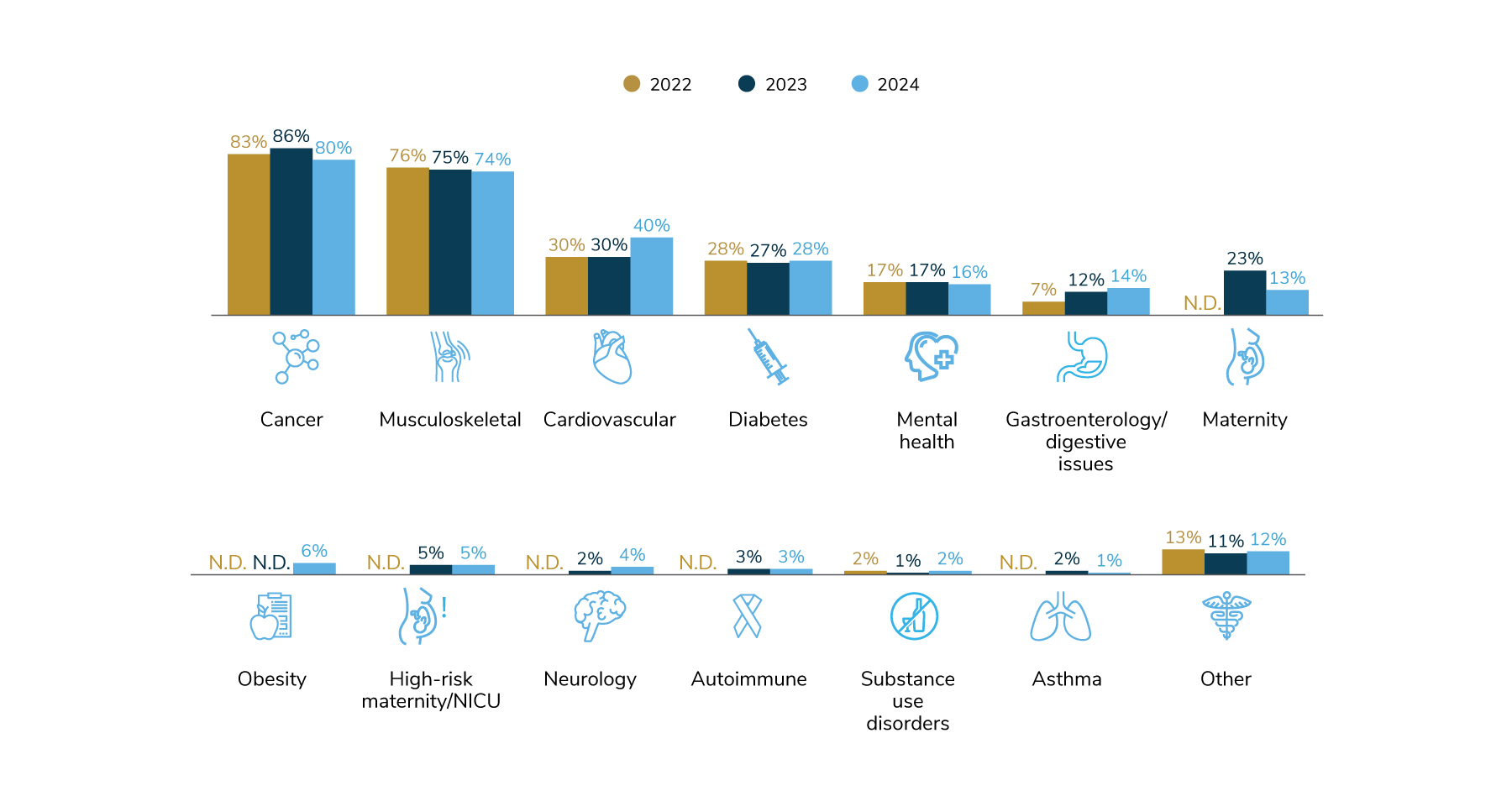

5 | Cancer remains the top condition driving cost; however, more employers say that cardiovascular conditions are among their top three cost drivers.

Concerns about the cost of cancer care may be further fueled by increased prevalence in younger populations. Furthermore, the growing cost of cancer treatments, including gene and cell therapies currently in the pipeline, leaves employers questioning how their plans will be impacted. While it is imperative that employers adopt strategies to address treatment cost, it is equally important that they amplify efforts to increase cancer prevention and early detection via screening approaches. Beyond cancer, employers continue to note musculoskeletal conditions as a cost concern. In addition, 40% of employers put cardiovascular conditions as their #3 cost driver, up from 30% in 2023.

Figure 8: Conditions Driving Cost, 2022-2024

Figure 8: Conditions Driving Cost, 2022-2024 -

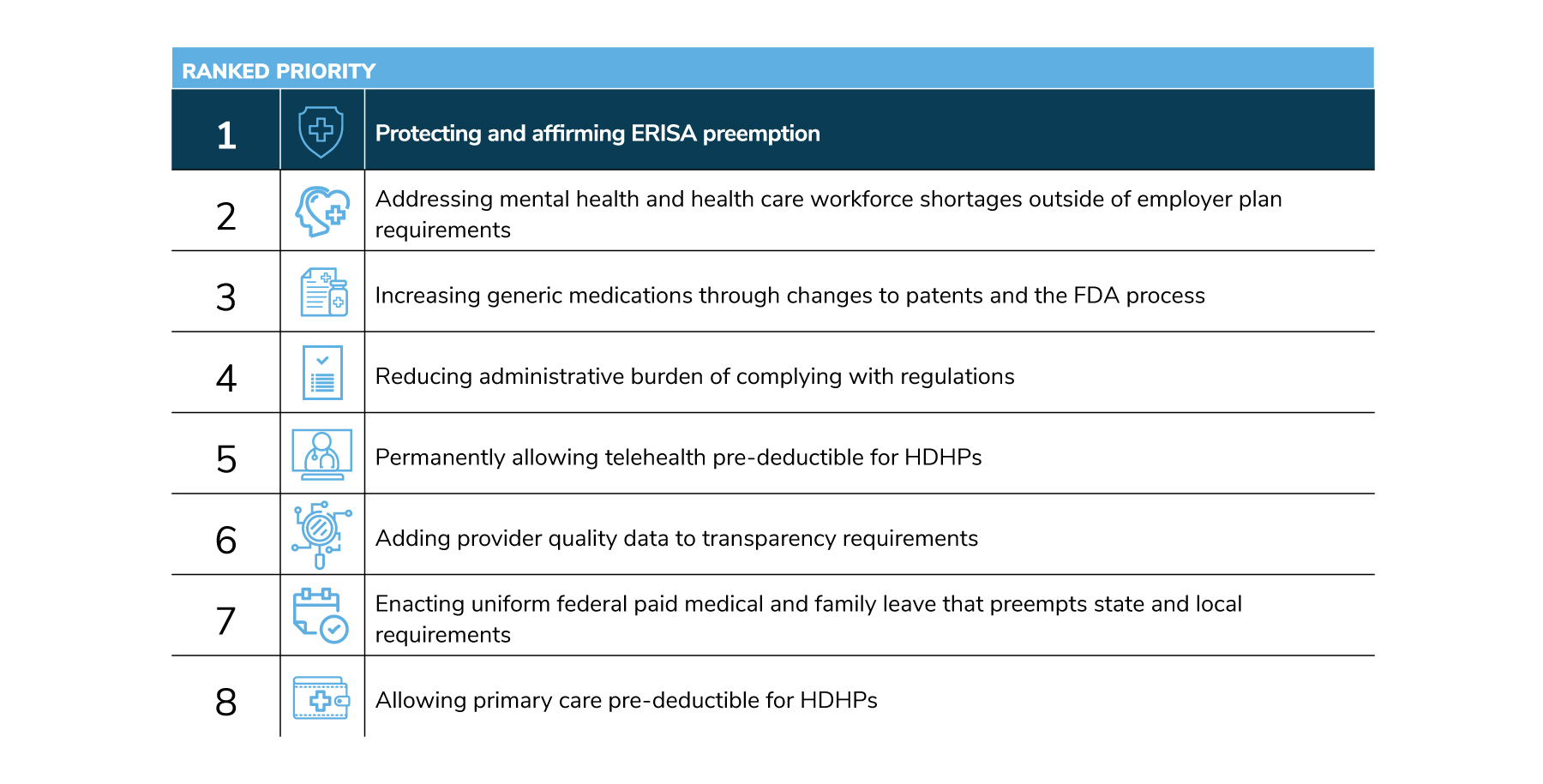

6 | Protecting ERISA preemption is employers’ highest priority for the Administration and Congress.

This finding reflects the importance of ERISA to employers, which allows them to offer their employees comprehensive benefits in a nationally consistent and competitive manner. Employers also prioritize addressing mental health and health care workforce shortages and increasing generic medication availability. Table 1 depicts the policy priorities based on average ranking of the employer respondents.

Table 1: Prioritized Efforts for the Administration and Congress, 2024

Table 1: Prioritized Efforts for the Administration and Congress, 2024 -

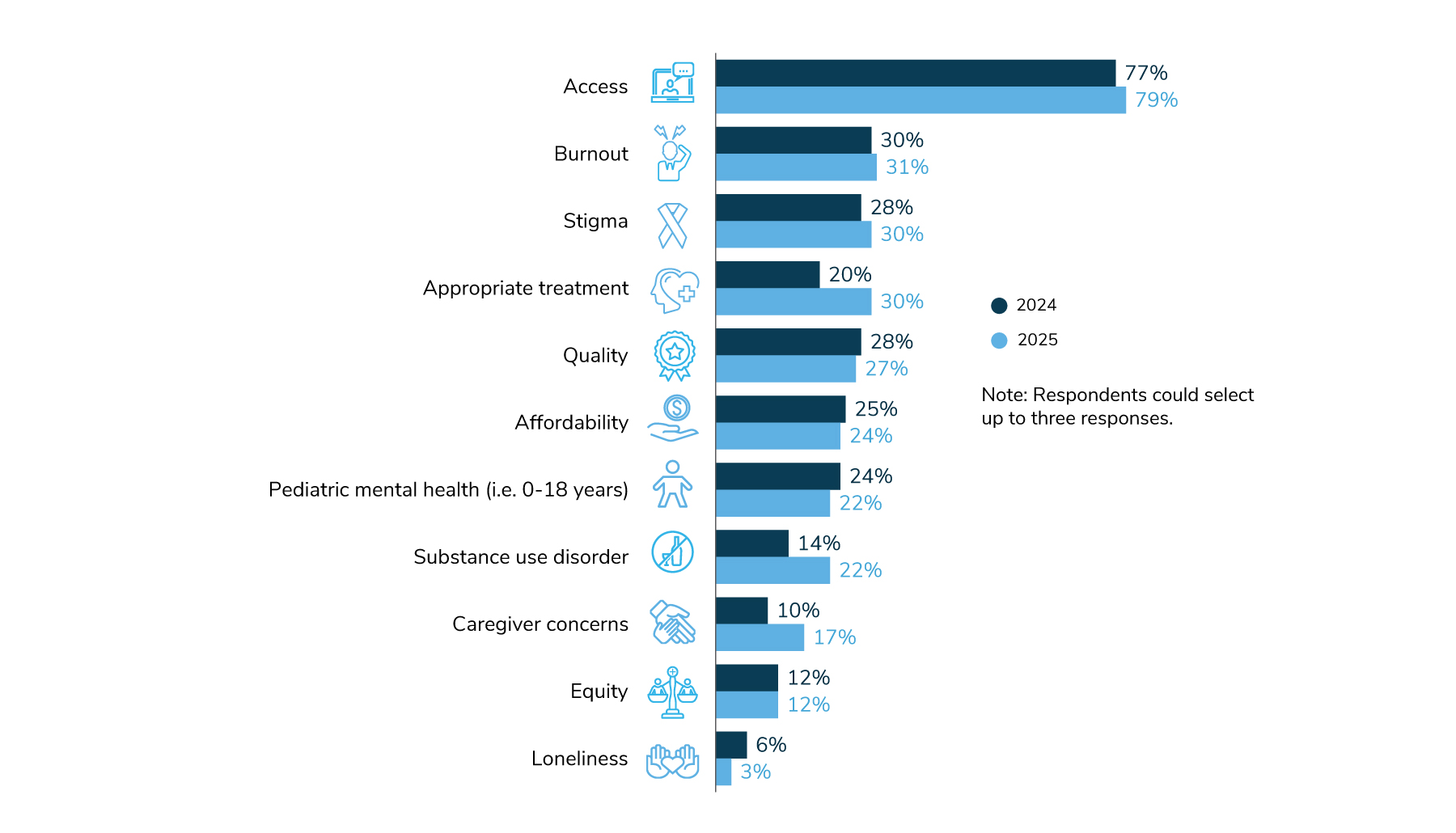

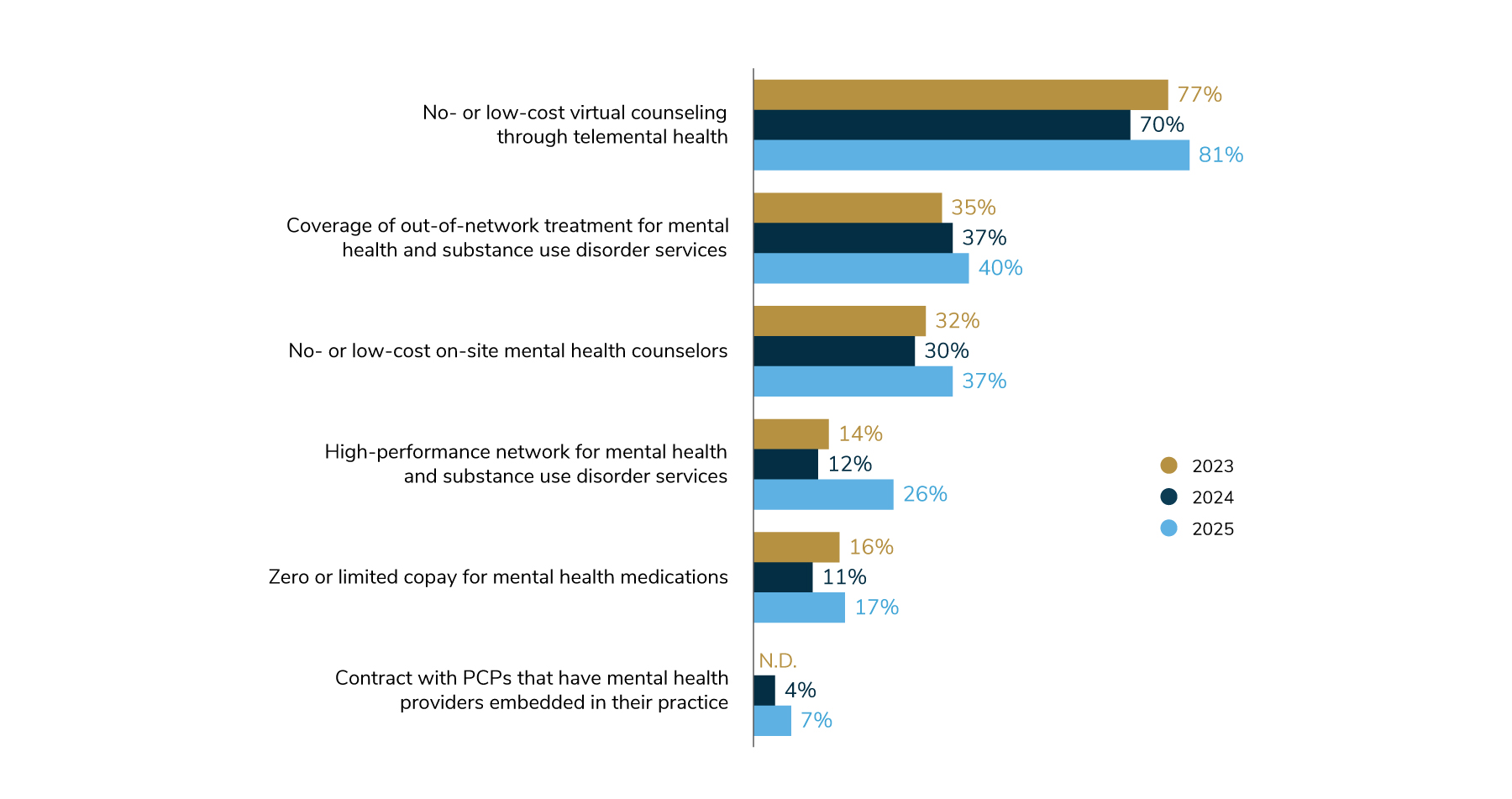

7 | Mental health continues to be a priority for employers, with a focus on access and ways to eliminate cost barriers.

Seventy-nine percent of employers say that access is one of their top three mental health priorities for 2025. To address access and costs, employers continue to pursue strategies, such as virtual counseling, eliminating out-of-network barriers and using on-site counselors.

Figure 9: Mental Health Priorities, 2024-2025

Figure 9: Mental Health Priorities, 2024-2025

Figure 10: Approaches to Improve Mental Health Access, 2023-2025

Figure 10: Approaches to Improve Mental Health Access, 2023-2025 -

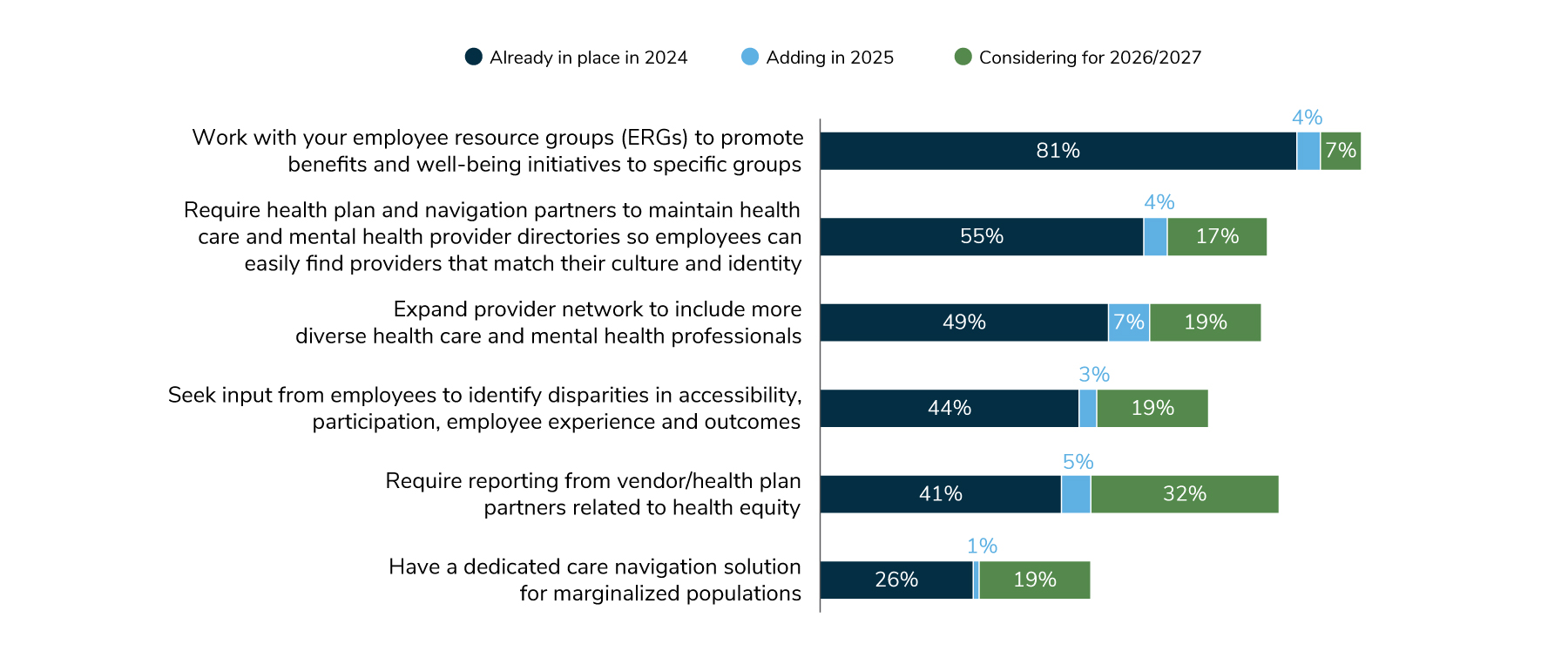

8 | Employers remain committed to health equity efforts that address disparities.

Employers continue to pursue a number of targeted approaches to narrow health disparities within their plans and programs. Holistically, the most common tactic found in the survey is collaborating with employee resource groups (ERGs) to promote benefits and well-being initiatives to specific groups. Employers are also drilling down on equity in four key areas: affordability issues for lower income employees; supporting LGBTQ+ employees’ health needs; women’s and reproductive health; and supporting those with a disability or who are neurodiverse.

Figure 11: Addressing Health Inequities Within Health and Well-being Programs, 2024-2027

Figure 11: Addressing Health Inequities Within Health and Well-being Programs, 2024-2027

Citations

Before referring to or using this survey report in any way, you must receive permission from Business Group on Health. Please contact [email protected].

Suggested citation for this survey report:

Business Group on Health. 2025 Employer Health Care Strategy Survey. August 2024. Available at: https://www.businessgrouphealth.org/resources/2025-Employer-Health-Care-Strategy-Survey-Intro.

-

Intro2025 Employer Health Care Strategy Survey

-

Executive SummaryExecutive Summary

-

Part 1Perspectives on Health Care

-

Part 2Health Care Costs

-

Part 3Vendors and Partnerships

-

Part 4Health Care and Mental Health Design

-

Part 5Pharmacy Costs and Management

-

Part 6Health Care Delivery

-

Part 7Health Equity

-

Part 8In Conclusion: 2025 Priorities

-

Full ReportFull Report

-

Chart PackChart Pack